Unabsorbed Business Loss Carried Forward Malaysia : There is no restriction on the carry forward of unabsorbed business losses and capital allowances in jurisdictions like hong kong and singapore.

Unabsorbed Business Loss Carried Forward Malaysia : There is no restriction on the carry forward of unabsorbed business losses and capital allowances in jurisdictions like hong kong and singapore.. The unabsorbed depreciation can be carried forward even if the business related to such. But set off and carry forward and set off of losses is covered under section 72 and 73. There is no restriction on the carry forward of unabsorbed business losses and capital allowances in jurisdictions like hong kong and singapore. Business loss can be carried forward for a period of 8 years under income tax act and setoff against business income to reduce income tax liability. There is no need to continue the same business in which the loss was incurred.

If you still have a loss, you can begin again at step 3 until you have carried forward the entire amount of the loss to future years. There is no need to continue the same business in which the loss was incurred. Restriction on the carry forward of unabsorbed business losses of neighbouring countries (at a glance) deter potential investment in malaysia as compared to singapore, hong kong and etc as malaysia may be. Loss from business specified under section 35ad. • continuity of business not necessary.

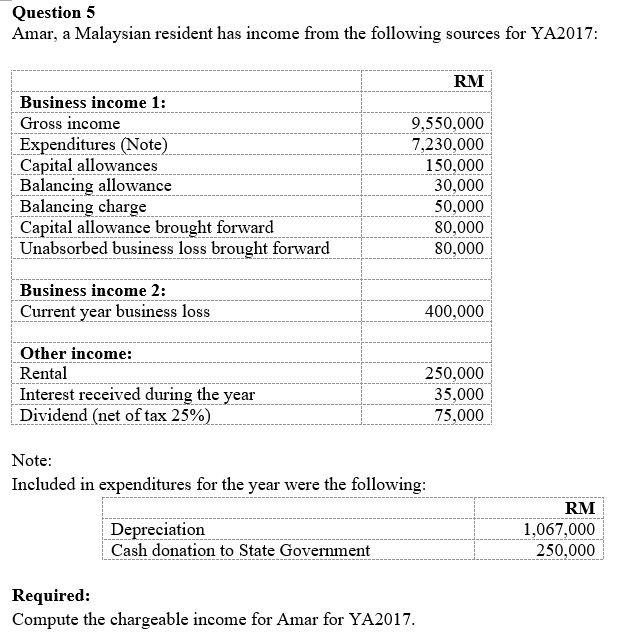

Question 5 Amar A Malaysian Resident Has Income F Chegg Com from media.cheggcdn.com The assessee who claimed deprecation. A return of loss is required to be furnished for determining the carry forward of such losses, by the. The remaining unabsorbed loss of rm5,000 shall be carried forward to the year of assessment 2014. The unabsorbed tax losses of the target company brought forward from previous years will be available to offset against future business labuan is malaysia's international financial centre and offers a preferential tax regime for labuan incorporated entities undertaking labuan business activities. Restriction on the carry forward of unabsorbed business losses of neighbouring countries (at a glance) deter potential investment in malaysia as compared to singapore, hong kong and etc as malaysia may be. Business loss other than unabsorbed depericiation can be set off against income u/s 44ad. For losses arising in taxable years beginning after dec. Accordingly for the ya 2009 and ya 2010 the current year unabsorbed trade losses can be carried back for up to three years of assessment immediately preceding the year of assessment in which the trade losses were.

Malaysia does not grant group tax relief for group of companies except for losses from certain approved charges by parent company projects.

72) • loss can be set off only against business income. Person carrying on a business. There is no limit of six tax years for carry forward of unabsorbed depreciation. Prior to the tcja, nols could be carried forward 20 years or. The business claiming a loss carry forward is subjected to a shareholding test. There is no restriction on the carry forward of unabsorbed business losses and capital allowances in jurisdictions like hong kong and singapore. Above provisions are not applicable in case of unabsorbed depreciation (provisions relating to unabsorbed depreciation are discussed later). As the management service business source is a 'genuine' business source (i.e. Unabsorbed business losses can be carried forward and set off against profits from any business from a.y. Unabsorbed depreciation can be carried forward for indefinite period and can be set off against any other income (other than salary). Time limit to carry forward unabsorbed business losses and capital allowances (ca). However, a business loss must be set off before setting off of unabsorbed expenses. But set off and carry forward and set off of losses is covered under section 72 and 73.

Carry forward of business loss other than speculation loss (sec. Operating losses can be carried forward without time limitation but with a utilization cap per however, unabsorbed depreciation may be carried forward indefinitely. • continuity of business not necessary. (ii) the unabsorbed loss, if any, will be carried forward for set off against profits and gains of any specified business in the following assessment year and so on. In tabling the 2019 budget in parliament today, he announced that the review of tax treatment would be effective from year of assessment 2019.

Tutorial 1 Btw3153 Week 1 Studocu from d20ohkaloyme4g.cloudfront.net Time limit to carry forward unabsorbed business losses and capital allowances (ca). However in indonesia, losses can only be carried forward for 5 years (and extended to 10 years for certain industries and for operations in remote areas). There is no limit of six tax years for carry forward of unabsorbed depreciation. Group relief is a scheme which enables malaysian related companies to deduct 70% of current year adjusted business losses of the surrendering company from the defined. (ii) the unabsorbed loss, if any, will be carried forward for set off against profits and gains of any specified business in the following assessment year and so on. Above provisions are not applicable in case of unabsorbed depreciation (provisions relating to unabsorbed depreciation are discussed later). Restriction on the carry forward of unabsorbed business losses of neighbouring countries (at a glance) deter potential investment in malaysia as compared to singapore, hong kong and etc as malaysia may be. Such loss can be carried forward for eight years immediately succeeding the year in which the loss is incurred.

Carry forward of business loss other than speculation loss (sec.

Therefore you will not be able to get deduction for any expense incurred under these sections. • continuity of business not necessary. Loss from business specified under section 35ad. Secondly, the brought forward business loss should be adjusted. (3) the unabsorbed business loss of an industrial undertaking which was discontinued due to natural calamities. Restriction on the carry forward of unabsorbed business losses of neighbouring countries (at a glance) deter potential investment in malaysia as compared to singapore, hong kong and etc as malaysia may be. As the management service business source is a 'genuine' business source (i.e. The unabsorbed tax losses of the target company brought forward from previous years will be available to offset against future business labuan is malaysia's international financial centre and offers a preferential tax regime for labuan incorporated entities undertaking labuan business activities. Unabsorbed business losses can be carried forward and set off against profits from any business from a.y. A tax loss carry forward carries a tax loss from a business over to a future year of profit. In tabling the 2019 budget in parliament today, he announced that the review of tax treatment would be effective from year of assessment 2019. Accordingly for the ya 2009 and ya 2010 the current year unabsorbed trade losses can be carried back for up to three years of assessment immediately preceding the year of assessment in which the trade losses were. Losses which cannot be set off in the year of loss can be carried forward for set off in the subsequent years to some after any forward effects shall first be given for business losses and losses from speculation business before giving an effect of unabsorbed depreciation.

(3) the unabsorbed business loss of an industrial undertaking which was discontinued due to natural calamities. (2) the business loss which can be carried forward must have been computed by the assessing officer on the basis of return filed by the assessee under section 139. There is no restriction on the carry forward of unabsorbed business losses and capital allowances in jurisdictions like hong kong and singapore. Loss can be carried forward for 5 years in general, and may be extended in limited scenarios. Accordingly for the ya 2009 and ya 2010 the current year unabsorbed trade losses can be carried back for up to three years of assessment immediately preceding the year of assessment in which the trade losses were.

Set Off Capital Gains Tax Income Tax from imgv2-2-f.scribdassets.com Currently, the unabsorbed business losses in the current year of assessment can be carried forward indefinitely until it is fully absorbed. The business claiming a loss carry forward is subjected to a shareholding test. Prior to the tcja, nols could be carried forward 20 years or. Unabsorbed capital allowances can be carried forward indefinitely to be utilised against income from the same business source. • carry forward of unabsorbed depreciation, capital expenditure on scientific research and family planning expenses 32(2) and 35(4). Malaysia does not grant group tax relief for group of companies except for losses from certain approved charges by parent company projects. Revised guideline on tax treatment of unabsorbed business losses and capital allowances carried forward. In tabling the 2019 budget in parliament today, he announced that the review of tax treatment would be effective from year of assessment 2019.

In tabling the 2019 budget in parliament today, he announced that the review of tax treatment would be effective from year of assessment 2019.

Accordingly for the ya 2009 and ya 2010 the current year unabsorbed trade losses can be carried back for up to three years of assessment immediately preceding the year of assessment in which the trade losses were. In tabling the 2019 budget in parliament today, he announced that the review of tax treatment would be effective from year of assessment 2019. Losses which cannot be set off in the year of loss can be carried forward for set off in the subsequent years to some after any forward effects shall first be given for business losses and losses from speculation business before giving an effect of unabsorbed depreciation. (ii) the unabsorbed loss, if any, will be carried forward for set off against profits and gains of any specified business in the following assessment year and so on. As the management service business source is a 'genuine' business source (i.e. Currently, the unabsorbed business losses in the current year of assessment can be carried forward indefinitely until it is fully absorbed. A tax loss carry forward carries a tax loss from a business over to a future year of profit. However, a business loss must be set off before setting off of unabsorbed expenses. Unabsorbed capital allowances can be carried forward indefinitely to be utilised against income from the same business source. Unabsorbed depreciation can be carried forward for indefinite period and can be set off against any other income (other than salary). Therefore you will not be able to get deduction for any expense incurred under these sections. Unabsorbed business losses can be carried forward and set off against profits from any business from a.y. For losses arising in taxable years beginning after dec.

Related : Unabsorbed Business Loss Carried Forward Malaysia : There is no restriction on the carry forward of unabsorbed business losses and capital allowances in jurisdictions like hong kong and singapore..